Hướng dẫn về thuế đối với hoạt động Affiliate Marketing tại Việt Nam

- Thứ tư - 11/06/2025 18:30

- In ra

- Đóng cửa sổ này

Affiliate marketing đang bùng nổ mạnh mẽ tại Việt Nam, mở ra cơ hội kiếm tiền hấp dẫn cho nhiều cá nhân và doanh nghiệp. Tuy nhiên, việc nắm rõ các quy định về thuế đối với hoạt động này là vô cùng quan trọng để đảm bảo tuân thủ pháp luật và tránh những rủi ro không đáng có. Bài viết này sẽ cung cấp cái nhìn toàn diện về nghĩa vụ thuế đối với Affiliate marketing, giúp bạn dễ dàng thực hiện đúng quy định.

1. Affiliate marketing là gì?

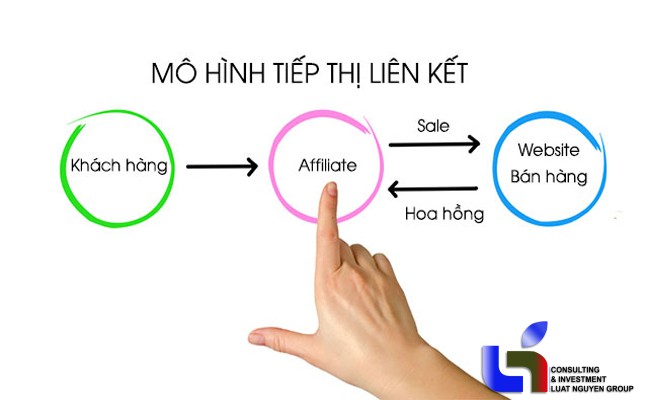

Affiliate marketing (tiếp thị liên kết) là một mô hình kinh doanh trực tuyến, trong đó cá nhân hoặc tổ chức (gọi là "Affiliate" hoặc "Publisher") quảng bá sản phẩm, dịch vụ của người khác (gọi là "Advertiser" hoặc "Merchant") thông qua các kênh trực tuyến như website, blog, mạng xã hội, email marketing, v.v. Khi có khách hàng thực hiện hành động cụ thể như mua hàng, đăng ký dịch vụ, điền form,... thông qua liên kết của Affiliate, Affiliate sẽ nhận được hoa hồng từ Advertiser.

Bản chất của hoạt động Affiliate marketing là cung cấp dịch vụ trung gian, môi giới, hoặc quảng cáo, xúc tiến thương mại trên môi trường mạng. Do đó, thu nhập từ Affiliate marketing là đối tượng chịu thuế theo quy định của pháp luật Việt Nam.

2. Hoạt động môi giới trực tuyến (Affiliate marketing) nộp thuế như thế nào?

Hoạt động Affiliate marketing tạo ra thu nhập cho cá nhân hoặc tổ chức, do đó, thu nhập này phải chịu thuế theo quy định của pháp luật thuế Việt Nam. Việc xác định loại thuế và cách thức nộp thuế sẽ phụ thuộc vào hình thức pháp lý của chủ thể thực hiện hoạt động Affiliate marketing (cá nhân không đăng ký kinh doanh, hộ kinh doanh, hay doanh nghiệp).

2.1. Cá nhân không đăng ký kinh doanh (Affiliate cá nhân)

Cá nhân không đăng ký kinh doanh, có thu nhập từ Affiliate marketing, sẽ được xem là cá nhân kinh doanh theo quy định của pháp luật thuế. Thu nhập này sẽ chịu thuế thu nhập cá nhân (TNCN) và có thể bao gồm cả thuế giá trị gia tăng (GTGT) nếu doanh thu vượt ngưỡng chịu thuế GTGT.

- Thuế TNCN: Thu nhập từ Affiliate marketing được xếp vào loại thu nhập từ kinh doanh.

- Phương pháp tính thuế: Thuế TNCN đối với cá nhân kinh doanh thường được tính theo phương pháp khoán (nếu không xác định được doanh thu, chi phí hoặc xác định được nhưng không đầy đủ), hoặc theo tỷ lệ phần trăm trên doanh thu (đối với trường hợp xác định được doanh thu).

- Tỷ lệ thuế TNCN: Theo Biểu thuế suất toàn phần đối với thu nhập từ kinh doanh quy định tại Khoản 2 Điều 10 Thông tư 111/2013/TT-BTC (sửa đổi, bổ sung bởi Thông tư 92/2015/TT-BTC), tỷ lệ thuế TNCN áp dụng là 0.5% trên doanh thu.

- Thuế GTGT: Cá nhân có doanh thu từ kinh doanh từ 100 triệu đồng/năm trở lên thuộc diện phải nộp thuế GTGT.

- Tỷ lệ thuế GTGT: Tỷ lệ thuế GTGT áp dụng đối với hoạt động dịch vụ (môi giới, quảng cáo) là 5% trên doanh thu.

- Tổng số thuế phải nộp: Là tổng của thuế TNCN và thuế GTGT. Công thức chung:

- Thuế phải nộp = Doanh thu tính thuế GTGT x Tỷ lệ thuế GTGT + Doanh thu tính thuế TNCN x Tỷ lệ thuế TNCN.

- Trong đó, doanh thu tính thuế GTGT và doanh thu tính thuế TNCN là doanh thu bao gồm thuế của toàn bộ tiền bán hàng, tiền gia công, tiền hoa hồng, phí dịch vụ phát sinh trong kỳ tính thuế từ các hoạt động sản xuất, kinh doanh hàng hóa, dịch vụ.

2.2. Hộ kinh doanh, cá nhân kinh doanh (đã đăng ký kinh doanh)

Đối với hộ kinh doanh, cá nhân kinh doanh đã đăng ký kinh doanh và có mã số thuế, việc nộp thuế sẽ tuân thủ các quy định hiện hành đối với hộ kinh doanh và cá nhân kinh doanh. Các khoản thuế chính bao gồm:

- Thuế môn bài: Nộp theo bậc môn bài dựa trên doanh thu.

- Thuế GTGT: Theo phương pháp khoán hoặc kê khai, tỷ lệ 5% trên doanh thu đối với hoạt động dịch vụ.

- Thuế TNCN: Theo phương pháp khoán hoặc kê khai, tỷ lệ 0.5% trên doanh thu đối với hoạt động kinh doanh.

- Nguyên tắc tính thuế: Hộ kinh doanh, cá nhân kinh doanh nộp thuế theo phương pháp khoán nếu không nộp theo phương pháp kê khai.

3. Hồ sơ khai, nộp thuế

3.1. Hồ sơ khai, nộp thuế đối với cá nhân không đăng ký kinh doanh

Cá nhân có thu nhập từ Affiliate marketing thuộc diện cá nhân kinh doanh nộp thuế theo phương pháp khoán thường không phải nộp tờ khai thuế định kỳ nếu đáp ứng điều kiện về doanh thu và không có yêu cầu khai báo khác. Tuy nhiên, trong một số trường hợp, cơ quan thuế có thể yêu cầu khai báo hoặc nộp hồ sơ khi có phát sinh thu nhập.

- Trường hợp cá nhân nhận hoa hồng thông qua một tổ chức: Tổ chức chi trả hoa hồng có trách nhiệm khấu trừ thuế TNCN tại nguồn theo tỷ lệ 10% (nếu thu nhập từ 2 triệu đồng/lần trở lên và cá nhân không có cam kết đủ điều kiện giảm trừ gia cảnh). Cá nhân không cần phải tự khai nộp thuế nếu thu nhập đã bị khấu trừ tại nguồn và không có thu nhập khác.

- Trường hợp cá nhân trực tiếp nhận thu nhập từ nước ngoài hoặc từ các nền tảng/công ty không thực hiện khấu trừ: Cá nhân phải tự khai và nộp thuế theo quy định về cá nhân kinh doanh. Hồ sơ khai thuế thường bao gồm:

- Tờ khai thuế (theo mẫu quy định của Bộ Tài chính).

- Các giấy tờ chứng minh thu nhập.

3.2. Hồ sơ khai, nộp thuế đối với hộ kinh doanh, cá nhân kinh doanh

Hộ kinh doanh, cá nhân kinh doanh nộp thuế theo phương pháp khoán sẽ được cơ quan thuế thông báo số thuế phải nộp và không phải nộp tờ khai thuế hàng tháng/quý. Tuy nhiên, họ vẫn phải thực hiện các nghĩa vụ sau:

- Nộp tờ khai thuế ban đầu: Khi bắt đầu hoạt động kinh doanh.

- Nộp tờ khai thuế khi có thay đổi: Doanh thu khoán, ngành nghề kinh doanh, địa điểm kinh doanh...

- Nộp tiền thuế theo thông báo của cơ quan thuế: Thường là nộp theo quý hoặc theo năm.

Đối với hộ kinh doanh, cá nhân kinh doanh nộp thuế theo phương pháp kê khai (áp dụng cho các trường hợp doanh thu lớn, có quy mô kinh doanh lớn, hoặc tự nguyện kê khai), hồ sơ khai thuế bao gồm:

- Tờ khai thuế GTGT (Mẫu số 01/GTGT).

- Tờ khai thuế TNCN (Mẫu số 01/CNKD).

- Bảng kê khai hóa đơn, chứng từ hàng hóa, dịch vụ mua vào, bán ra (nếu có).

4. Thời hạn phải nộp hồ sơ khai thuế

- Đối với cá nhân kinh doanh nộp thuế theo phương pháp khoán (cá nhân không đăng ký kinh doanh):

- Trường hợp tự khai nộp thuế: Thời hạn nộp hồ sơ khai thuế là ngày cuối cùng của tháng đầu tiên của quý phát sinh nghĩa vụ thuế, hoặc theo thông báo của cơ quan thuế.

- Trường hợp tổ chức chi trả khấu trừ tại nguồn: Tổ chức chi trả thực hiện việc kê khai và nộp thuế theo quy định đối với thu nhập từ tiền lương, tiền công.

- Đối với hộ kinh doanh, cá nhân kinh doanh (đã đăng ký kinh doanh):

- Nộp thuế theo phương pháp khoán: Không phải nộp hồ sơ khai thuế định kỳ, chỉ nộp tiền thuế theo thông báo của cơ quan thuế.

- Nộp thuế theo phương pháp kê khai:

- Khai thuế theo quý: Chậm nhất là ngày 30 của tháng đầu tiên của quý tiếp theo quý phát sinh nghĩa vụ thuế.

- Khai thuế theo năm: Chậm nhất là ngày cuối cùng của tháng thứ 3 kể từ ngày kết thúc năm dương lịch hoặc năm tài chính.

5. Xử phạt vi phạm hành chính do chậm nộp hồ sơ khai thuế

Cá nhân, hộ kinh doanh chậm nộp hồ sơ khai thuế sẽ bị xử phạt vi phạm hành chính theo quy định tại Nghị định 125/2020/NĐ-CP ngày 19/10/2020 của Chính phủ quy định xử phạt vi phạm hành chính về thuế, hóa đơn. Mức phạt cụ thể như sau:

- Phạt cảnh cáo: Chậm nộp từ 01 đến 05 ngày nếu có tình tiết giảm nhẹ.

- Phạt tiền từ 2.000.000 đồng đến 5.000.000 đồng: Chậm nộp từ 01 ngày đến 30 ngày (trừ trường hợp phạt cảnh cáo).

- Phạt tiền từ 5.000.000 đồng đến 8.000.000 đồng: Chậm nộp từ 31 ngày đến 60 ngày.

- Phạt tiền từ 8.000.000 đồng đến 15.000.000 đồng: Chậm nộp từ 61 ngày đến 90 ngày.

- Phạt tiền từ 15.000.000 đồng đến 25.000.000 đồng: Chậm nộp từ 91 ngày trở lên hoặc có hành vi trốn thuế, gian lận thuế.

Ngoài ra, cá nhân, hộ kinh doanh còn phải nộp tiền chậm nộp thuế (nếu có) tính trên số tiền thuế chậm nộp theo quy định.

Chú ý:

Các thông tin trên mang tính chất tham khảo và có thể thay đổi theo quy định của pháp luật tại từng thời điểm. Để đảm bảo tuân thủ đúng và đủ các nghĩa vụ thuế, bạn nên tham khảo ý kiến của chuyên gia tư vấn thuế hoặc liên hệ trực tiếp với cơ quan thuế địa phương. Việc chủ động nắm bắt và thực hiện đúng nghĩa vụ thuế không chỉ giúp bạn tránh được các rủi ro pháp lý mà còn góp phần xây dựng môi trường kinh doanh minh bạch, lành mạnh.

Xem thêm >>>

Các tin khác

luatnguyen.com

--------

BBT Luật Nguyễn